TECH6 WEBINAR IFRS 16 Entenda o impacto da norma nas Operadoras de Plano de Saúde

In the initial recognition of lease liability, variable lease payments are measured using the actual value of an index or a rate at the commencement date (IFRS 16.27 (b)). This implies that the lessee cannot use forward rates or forecasting techniques in measuring variable lease payments (IFRS 16.BC166). Variable payments that are independent.

IFRS IN PRACTICE IFRS 16 Leases

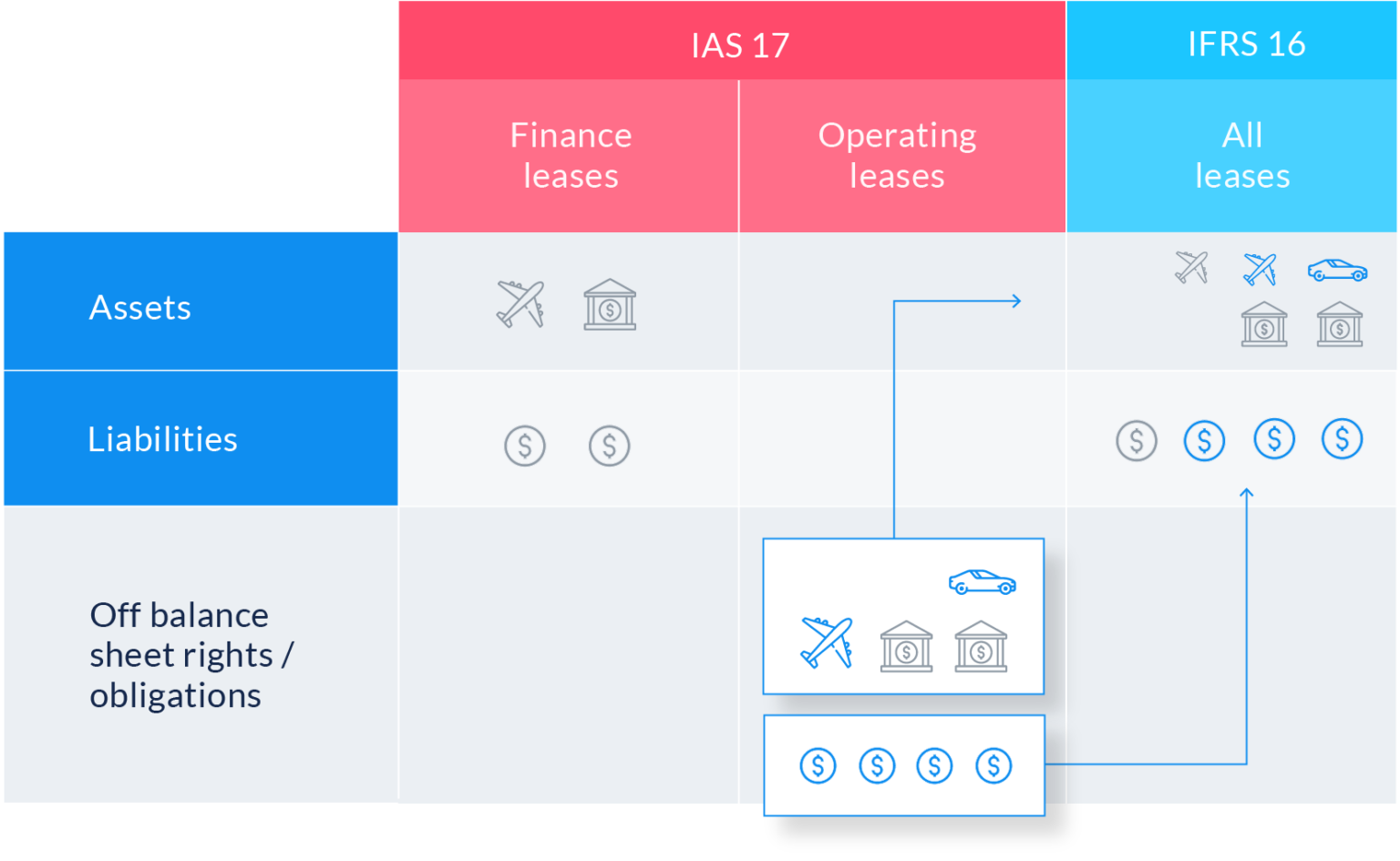

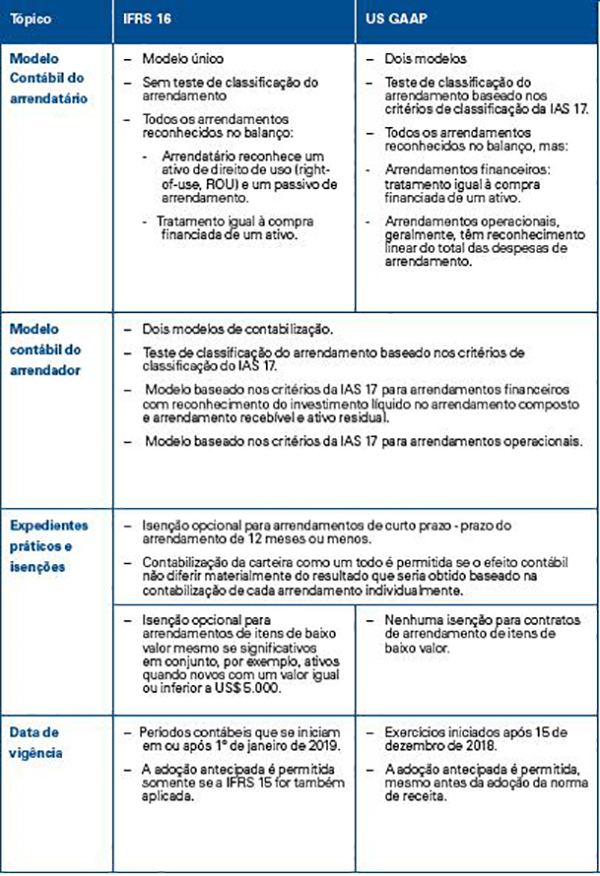

Some of these Day Two accounting differences are driven by the use of a single on-balance sheet lease accounting model under IFRS Standards as compared with a dual classification on-balance sheet lease accounting model under US GAAP (i.e. finance leases and operating leases). IFRS 16 effectively treats all on-balance sheet leases as finance.

IFRS 16 Lease Accounting Software EZLease

1 IFRS 16 at a glance 1.1 Key facts This publication provides an overview of IFRS 16 and how it affects the financial statements of the lessee and the lessor. It includes examples and insights. The publication begins with an overview of the lessee and lessor accounting models, summarising the impact of IFRS 16 on their respective financial

Leases IFRS 16

The application of IFRS 16.C10(c) is tantamount to treating the leases as short-term leases from the DIA. Accordingly, Entity B applies the guidance in IFRS 16.5-8 to such leases. In accordance with IFRS 16.7(a), when a short-term lease is modified, the lease is considered to be a new lease on the effective date of the modification.

Brilliant Ifrs 16 Template Excel Quotation Format In Gst

Presentation and disclosure. 31 Jul 2019. IFRS 16 requires lessees and lessors to provide information about leasing activities within their financial statements. The Standard explains how this information should be presented on the face of the statements and what disclosures are required. In this article we identify the requirements and provide.

IFRS 16 Transcendental cambio en la normativa contable de arrendamientos IFE Conferencias

Benefits of AARO Lease IFRS 16: Simple monitoring of the effects of IFRS 16. Automatic calculations of tax, interest, etc. Keeps track of all your leases, start and end dates, etc. Easy to keep contracts with different currencies separate. The contracts are saved periodically, giving you complete traceability in changes and calculations.

IFRS 16 O que muda na análise do ativo? Dica de Hoje Research

An asset retirement obligation (ARO) is a legal obligation that is associated with the retirement of a tangible, long-term asset. It is generally applicable when a company is responsible for removing equipment or cleaning up hazardous materials at some agreed-upon future date. A company must realize the ARO for a long-term asset at the point an.

Editora Roncarati Entendimento sobre o IFRS 16 Operações de arrendamento mercantil Artigos

In January 2016 the Board issued IFRS 16 Leases. IFRS 16 replaces IAS 17, IFRIC 4, SIC-15 and SIC-27. IFRS 16 sets out the principles for the recognition, measurement, presentation and disclosure of leases. In May 2020 the Board issued Covid-19-Related Rent Concessions, which amended IFRS 16.

Ifrs 16 Leases A Simplified Summary Of Ifrs 16 With Practical Hot Sex Picture

Debit P/L - Finance Expenses: CU 39 (1 967*2%) Credit Provision for Decommissioning: CU 39. Now, let's say that in 20X3, your estimate of the discount rate changes to 1.8% and all the other estimates (cash flows) remain unchanged. You need to recalculate the provision and account for its changes under IFRIC 1.

IFRS 16 Lease Accounting Software EZLease

Asset retirement obligation under ASC 842, IFRS 16 and GASB 87. By Visual Lease January 30, 2020 Lease Accounting, Lease Administration, Lease Management. If you have signed an operating lease for space, built leasehold improvements, and determined that you are legally required to take out the leasehold improvement when the lease expires, then.

Adopting IFRS 16 What Is The Best Option For You? CPDbox Making IFRS Easy

3.4 Recognition and measurement (AROs) Asset retirement obligations are initially recognized as a liability at fair value, with a corresponding asset retirement cost (ARC) recognized as part of the related long-lived asset. Figure PPE 3-1 highlights accounting considerations over the life of an ARO; each phase is discussed in more detail in the.

Ifrs 16 new leases pwc IFRS 16 The leases standard is changing Are you ready? IFRS 16 The

In-depth application guidance on the new leasing standard. We have been releasing our in-depth application guidance on IFRS 16 Leases in manageable chunks, one chapter at a time. Each one focuses on a particular aspect and includes explanations of the requirements and examples showing them in practice, to help you apply the new standard.

IFRS 16 video 10a Eng YouTube

IFRS 16 is effective for annual periods beginning on or after 1 January 2019. Early application is permitted, provided the new revenue standard, IFRS 15 Revenue from Contracts with Customers, has been applied, or is applied at the same date as IFRS 16. IFRS 16 requires lessees to recognise most leases on their balance sheets.

IFRS 16 Leases raubt den OffBalanceVorteil für Leasingnehmer BankingHub

This course gives you the basics of the product AARO Lease IFRS 16, the tool that gives you control over your leasing contracts and the IFRS 16 effects in your group. The day ends with a review of basic AARO functionality and administration, which you need to use AARO Lease IFRS 16. This review is important for those who work with the.

IFRS 16 leases module 1 YouTube

14.1.8 Presentation and disclosure (ASC 842 and IFRS 16) For lessees, the presentation of the right-of-use assets and lease liabilities are similar under the standards. Amounts relating to leases are presented separate from other assets and liabilities on the balance sheet or in the notes to the financial statements.

IFRS 16 Leases Implications and Application IFRS 16 Leases Implications and

However IFRS allows ARO cost to be added to the carrying amount of inventories as is discussed in paragraph BC15 of IAS 16. Recognition of ARO The obligations for dismantling and restoration costs accounted for in accordance with Ind AS 2 or Ind AS 16 are recognised and measured in accordance with Ind AS 37, Provisions, Contingent Liabilities.